|

| Image by Willi Heidelbach from Pixabay.com. |

Low Volatility Investing:

What's missing from investors' analysis?

By Nicholas Alonso/PanAgora

Will the Low Volatility Premia Continue to Pay Off?

Competing theories on why Low Volatility premia payoff leave us uncertain about the continued alpha potential for these strategies in the near future. One common explanation for the existence of the Low Volatility premia is that Low Volatility stocks are underpriced because of agency friction experienced by asset allocators who look to move away from their capitalization-weighted benchmarks. The fact that such frictions are likely to persist is an argument for the continued existence of the Low Volatility premia.[1]

Conversely, PanAgora’s CIO of Multi Asset, Dr. Edward Qian, has suggested that the performance of Low Volatility stocks typically appears strongest before Federal Reserve monetary easing decisions, which typically occur during times of stress.[2] Low Volatility alpha may thus be a harbinger for downturns in the equity market. If this is the case, the recent performance of Low Volatility strategies may be considered near its end.

Precisely because it is so difficult to forecast the continued alpha generated by these strategies, we believe that the more pertinent factor when deciding to invest in Low Volatility strategies should be downside protection.

Devil Is in the Details: How Portfolio Construction Techniques Impact Downside Protection

Low Volatility strategies seek to provide downside protection by lowering the volatility of the equity portfolio. While this seems like an obvious investment objective there are, in fact, many periods where the general collection of low volatility portfolios did not provide the expected downside protection. The reason for dispersion amongst low-volatility portfolio performance in market downturns is that low volatility is a portfolio characteristic and not solely a stock characteristic. The volatility of a portfolio depends both on the stocks idiosyncratic volatility, but also a stocks co-movement with other stocks in the portfolio. Stocks with low correlations to other stocks can lower the volatility of a portfolio even if that stock has a high volatility. Diversification, therefore, is an important feature that is often ignored in low volatility portfolios.

The fact that low volatility is a portfolio characteristic leads to an important observation that there are many different ways to build a low volatility portfolio that each lead to very different performance results. PanAgora has analyzed the outcomes of several low volatility portfolio construction methodologies.

Our results show that performance of certain strategies, such as minimum variance and maximum diversification, are heavily dependent on which risk model is used as an input to the process. The variability in outcomes that result from simply changing the initial measurements of risk should give investors pause. We believe there is a better way to build low volatility portfolios. One that has shown to be robust to changes in the risk models and that leads to behaviors that are much more in line with the expectations for low-volatility investing.

|

| Click image to enlarge graph. |

January 1995 – June 2019. Backtest begins in January

1995 due to data availability. These backtest results presented are gross of

fees and are shown for illustrative purposes only. They do not represent actual

trading or the impact of material economic and market factors on PanAgora’s

decision-making process for an actual PanAgora client account. As with any

investment, there is the possibility of profit as well as the risk of loss.

Please see the disclosures at the end of this presentation. Source: PanAgora

A Path Forward: Risk Balanced Portfolio Construction

At PanAgora, we have focused the vast majority of our research efforts determining what is responsible for the unexpected results we see in different investment styles. We believe that these unexpected outcomes tend to be driven by a lack of true diversification.

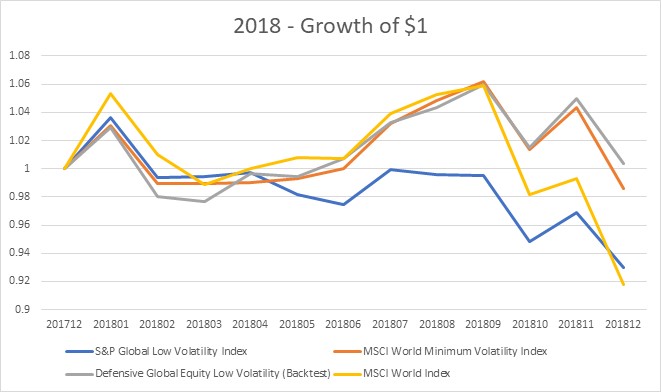

Risk balancing comes from a fundamental belief that “true” diversification is achieved by giving every investment in a portfolio an equal contribution to the risk of a portfolio.[3] We believe diversification in low volatility portfolios leads to outcomes that are both more robust and more in line the expectations of low volatility investing. Certain periods, such as Q4 2018, show that risk balanced portfolio construction may deliver on the expected outcome of low volatility portfolios, whereas other portfolio construction approaches have produced unexpected results.

|

| Click image to enlarge graph. |

Past performance is not a guarantee of

future results. Performance shown gross of fees. Please see the disclosures at

the end of this presentation. Source: PanAgora

BACKTESTED PERFORMANCE: The model and hypothetical performance included in the presentation does not represent the performance of actual client portfolios. The performance is shown for illustrative purposes only.

Resources:

[1] Baker, M., Bradley, B., & Wurgler, J. (2011). Benchmarks as Limits to Arbitrage: Understanding the Low-Volatility Anomaly. Financial Analysts Journal, 67(1). Retrieved from http://people.stern.nyu.edu/jwurgler/papers/faj-benchmarks.pdf

[2] Qian, E., & Qian, W. (n.d.). The Low-Volatility Anomaly, Interest Rates, and the Canary in a Coal Mine. The Journal of Portfolio Management , 43(4), 3–12.

[3] “On the Financial Interpretation of Risk Contribution: Risk Budgets Do Add Up.” Journal of Investment Management, Vol. 4, No. 4 (2006), pp. 41-51.

About the Author:

No comments:

Post a Comment