How to keep your balance if volatility returns in 2018

By Douglas J. Peebles and Matthew Sheridan

Guest Columnists

The volatility bond investors expected when 2017 began never showed up. We suspect it will come out of hiding in 2018. With valuations stretched and monetary policy turning, investors will want to think carefully about which risks they take.

This year was supposed to be the one that would shake up the status quo of modest growth, tepid inflation and low bond yields. The Federal Reserve did its part by raising interest rates and starting to reverse the asset purchases that created trillions of dollars of liquidity after the financial crisis.

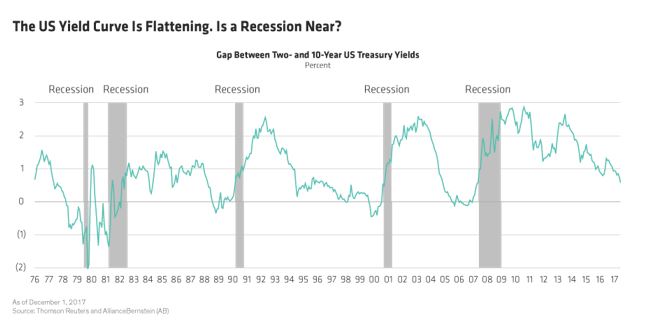

But the markets didn’t stick to the script. Risk assets such as equities and high-yield bonds have continued to rise and the US dollar has been falling. Long-term US Treasury yields, meanwhile, have declined and the yield curve, which plots the gap between two- and 10-year yields, has become flatter. In other words, financial conditions eased substantially—the opposite of what the Fed intended.

Why Is the Yield Curve Flattening?

A flattening yield curve is typically seen as a warning sign for markets. It suggests that growth is slowing and a recession may be near (Display). Is that what’s happening here? We don’t think so. At least, not yet.

If a recession were just around the corner, it would mean that the Fed has been tightening policy too quickly. But if that were the case, you would expect to see equity valuations take a hit and economic data to deteriorate. What’s more, the Fed’s benchmark interest rate—in nominal and real, or inflation-adjusted, terms—is still low and the curve is steeper than it was in the run-up to previous recessions.

So why are long-term yields so low? A more likely explanation, in our view, is that there’s still a tremendous amount of liquidity in the financial system. During and after the financial crisis, the Fed flooded the economy and markets with money and kept long-term rates low by buying trillions of dollars of bonds. That distorted many market signals. By letting some of the bonds on its balance sheet mature, the Fed has slowly started to drain that excess liquidity. But it has a long way to go.

At the same time, the Bank of Japan and European Central Bank are still buying bonds and other financial assets, which helps to offset the Fed’s modest tightening. Even so, a flatter yield curve can’t be dismissed outright. We think caution is warranted.

Don’t Count the Fed Out

Of course, none of this means yields will remain low forever. With the economy operating at full capacity, the Fed is widely expected to raise rates several times in 2018. If big changes to US tax policy become law and boost growth and inflation, the Fed may be forced to tighten even more aggressively.

This action would likely increase volatility and have implications for various sectors of the bond market. That’s why investors will have to be careful about how they manage their exposure to the market’s two primary risks—interest rates and credit.

Normally, return-seeking credit assets such as high-yield corporate bonds and emerging-market debt do well when growth accelerates and interest rates rise. Treasuries and other high-quality bonds—we like to call them risk-reducing assets—struggle in these conditions because higher rates and rising inflation reduce these securities’ market value. In such circumstances, investors may be tempted to reduce their interest-rate risk—or duration—and increase their credit risk.

Want Balance? Consider a Credit Barbell

But these aren’t normal times. Years of central bank asset purchases and low rates encouraged global investors to crowd into the same high-yielding credit assets. That’s raised valuations and compressed yield spreads—the extra yield they offer over comparable government bonds.

There are certainly still opportunities with credit markets, but we think investors should think twice about taking on too much credit risk, given current prices and conditions. A better approach, in our view, would be to pair Treasuries and other interest-rate-sensitive assets and growth-sensitive credit assets in a single strategy known as a credit barbell. Because the returns from the two types of assets are negatively correlated, strong returns on one side of the barbell can outweigh weakness on the other.

U.S. Treasuries, of course, will struggle over the short term if tighter Fed policy eventually causes the curve to steepen. But even in rising-rate environments, these assets provide crucial stability, diversification and income.

Exposure can also keep your bond portfolio liquid. Eventually, higher rates will slow growth and put an end to the credit cycle. In these periods, Treasuries tend to beat assets such as high-yield bonds. This means investors can rebalance their portfolios by selling outperforming US Treasuries and buying underperforming credit assets at discount prices.

The key to success, in our view, is having the ability to actively adjust your interest rate and credit weightings as conditions and valuations change. If markets do get more volatile in 2018, the balance will be more important than ever.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams or TEXPERS.

About the Authors:

|

| Douglas J. Peebles |

Douglas J. Peebles is the chief investment officer of AB Fixed Income and a Partner of the firm, focusing on fixed-income investment processes, strategy and performance across portfolios globally. As CIO, he is also co-chairman of the Interest Rates and Currencies Research Review team, which is responsible for setting interest-rate and currency policy for all fixed-income portfolios. In addition, Peebles serves as lead portfolio manager for AB’s Unconstrained Bond Strategy and focuses on managing the firm’s strategic client relationships.

|

| Matthew Sheridan |

Matthew Sheridan is a senior vice president and portfolio manager at AB, primarily focusing on the global multi-sector strategy portfolios. He is a member of the global fixed income, global high income and emerging market debt portfolio-management teams. Additionally, Sheridan is a member of the rates and currency research review team and the emerging market debt research review team.

No comments:

Post a Comment