Remastering volatility: Reducing noise in equity allocations

By Christopher Hogbin, Christopher Marx and Nelson Yu/Guest Contributors

Volatility is a challenge that has vexed equity investors for

decades, yet its root causes are often misunderstood. Understanding how a

company’s business profile determines a stock’s risk can help investors prepare

for uncertainty and make better decisions when market turbulence strikes.

Erratic market behavior often seems like a mystery. Bad economic

news, political chaos, interest-rate moves or an industry crisis can trigger

widespread anxiety among investors and inflict indiscriminate damage to

equities. This volatility is the admission price that investors must pay to

access the higher return potential of stocks and other risk assets. Yet

volatility also reduces returns through risk drag, and often prompts emotional,

financially destructive decisions that stem from the fear of loss.

Behind the headlines that incite volatility, market fluctuations

are ultimately driven by the collective behavior of individual stocks. And the

risk profile of a stock often stems from fundamental and researchable aspects

of its business model and strategy.

Confidence in Cash Flows—the Source of Risk

For individual stocks, the source of volatility is derived from

investor confidence in company cash flows. In finance textbooks, the value of

an asset is defined as a function of its future cash flows and the discount

rate, which itself is a function of interest rates. It’s also affected by the

perceived variability of a company’s cash-flow potential; greater uncertainty

around cash flows will raise the discount rate and lower a stock’s valuation.

So, anything that can provoke uncertainty around a company’s cash flows may

become a source of volatility. A company’s income statement may offer important

clues about its resilience or underlying vulnerabilities.

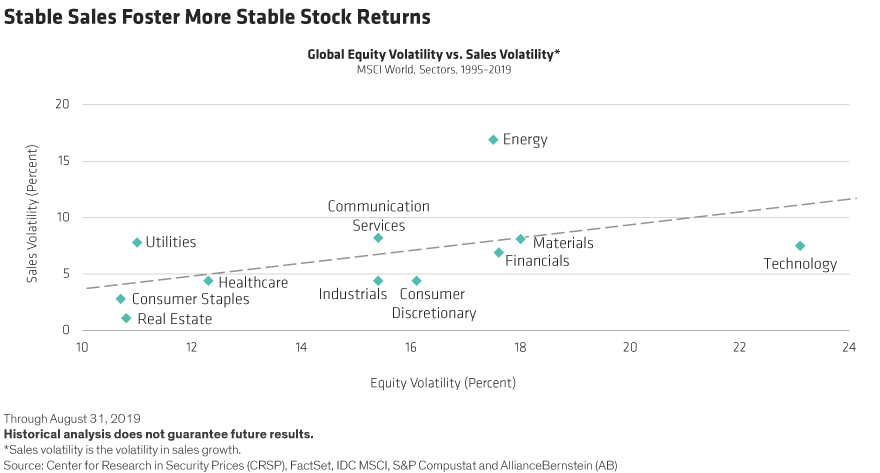

Let’s start at the top, with revenues. Sales are an important

driver of company earnings, but can be unpredictable. And sales volumes can be

very sensitive to changes in economic cycles in industries like autos and

retail; changes in supply/demand balances, which often get reflected in

changing prices for commodities, for example; and changes in competition or

technology, which can impact market shares. Other industries, such as consumer

staples and utilities, typically see more stable demand and pricing, and thus

more stable sales. Our research shows that sectors with more stable sales

patterns tend to be less volatile (See chart below).

|

| Click image to enlarge chart. |

Within any sector, understanding a company’s business model and forecasting its cash flows is the cornerstone of active equity investing. Just as important, fundamental research must also identify the risks to a company’s cash flows. Our research shows that companies with a higher volatility of cash flows also tend to have more volatile stock returns (see left chart, below). This means that the structure of a company’s business model can also be a source of volatility—and its income statement may offer important clues about its resilience or underlying vulnerabilities.

|

| Click image to enlarge charts. |

Cost Structures Matter

Cash flows can also be profoundly affected by cost structures. Consider two companies with very different cost structures. One requires little capital to get started, so it has low operating leverage. The other requires a much bigger investment to get started and has high operating leverage. The company with lower operating leverage starts out in a much more profitable position, while the company with higher operating leverage starts off with losses and will need to sell more units to become profitable (see right chart, above).

So how the company makes money can have a material impact on its

profitability and consistency. Industries that generally exhibit lower

operating leverage include services and retail. Companies with higher operating

leverage tend to have high fixed costs, either from large upfront capital

requirements in industries like mining and autos, or a fixed labor force. These

types of companies also tend to be more sensitive to the economic cycle and to

the changing tastes and habits of consumers.

Taking Calculated Risks, Avoiding Unintended Exposures

Of course, business models aren’t the only thing that determines a

company’s risk profile. Company debt positions (or leverage) and sensitivity to

exogenous shocks from the macroeconomy or politics will also influence the

volatility of its stock. In future blogs, we will examine other sources of

volatility and how to manage them. But we believe that with a clearer grasp of

the way company-specific risks are at the heart of a stock’s volatility, active

managers can better assess the risk-taking needed to achieve desired returns

and reduce noise that can undermine confidence in an allocation.

By understanding the sources of volatility, portfolio managers can

better drive their outcomes through intentional views—taking risk where insight

identifies an opportunity for improved returns, while controlling the

volatility of unintended exposures. This helps reduce the noise that interferes

with an investing plan, and is the key to remastering portfolios and realizing

the benefits of long-term equity returns.

This blog post is based on a whitepaper that was published in October

2019 titled Remastering Volatility:

Reducing Noise in Equity Allocations.

About the Authors:

No comments:

Post a Comment