A Case for Midstream Hybrids

By Shalin Patel, guest columnist

We view midstream hybrid securities as an attractive investment for enhancing yield (6-10 percent) and total return to a portfolio without taking on significant underlying equity volatility or commodity price uncertainty.

Hybrids are attractive to issuers since rating agencies assign them partial equity treatment, allowing companies to issue debt-like securities without jeopardizing their credit ratings. Hybrids provide investors with a better yield than the relevant issuer’s senior debt and a higher position in the capital structure compared to the equity along with positive correlation to interest rates (post coupon reset to a floating structure).

|

| Click image to enlarge. |

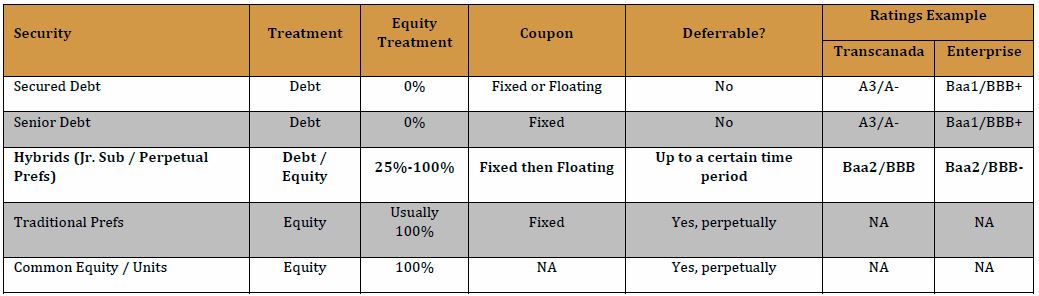

Hybrid Securities Overview

Hybrids have historically been utilized by Financial/Insurance and Banking issuers to lower their cost of capital and comply with the requirements of Basel 3 guidelines but have gained prominence amongst other sectors in recent years.

|

| Click image to enlarge. |

Since 2011, midstream companies have raised $126 billion in equity through unit issuance while raising $40 billion through hybrid issuance through 280 equity deals vs. 87 hybrid deals. However, the issuance of hybrids picked up significantly in 2016/2017 (52 equity deals vs. 44 hybrid deals) as the equity performance of midstream companies remained volatile.

|

| Click image to enlarge. |

Cost of Capital (MLPs vs. Hybrids)

Since 2011, midstream companies have issued $40 in hybrids with an average cost of capital differential of ~300bps (higher in 2015-2016) compared to equity yield. Given the recent rise in equity cost of capital for midstream companies and leverage concerns, we believe hybrids will continue to be a preferred avenue to raise capital.

|

| Click image to enlarge. |

|

| Click image to enlarge. |

Pros/Cons of Hybrids

- Solid Yield Differential: In our study, we found that hybrids are trading at a spread of +179bps (range of ~60bps to ~400bps) to their respective senior note’s yield-to-worst. In our view, this yield differential is significant given that an investor is not taking duration risk (unlike longer dated bonds) and the ratings differential is minor (1-2 notches below senior notes).

- Strong position in the capital structure: Unlike equity units where there is distribution/dividend cut risk, hybrid issuers cannot cut coupons. Hybrids do offer the issuer the option to defer interest for a certain period. However, in the event the issuer chooses to defer the interest on the hybrids, it is forbidden to pay any distribution/dividends or engage in any dividends.

- Positive correlation to interest rates: Hybrids have a floating rate component embedded in their coupon structure and usually float at LIBOR plus a fixed spread. Given the rising rate environment, hybrids offer investors an attractive way to earn a decent cash yield and rising correlation to interest rates without stepping out on the duration curve.

About the Author

Shalin Patel joined BlackGold Capital Management LP in 2010 and is the director of research, overseeing the research efforts of the investment team while covering the Midstream sector. Mr. Patel also serves on the Investment and Risk Management Committees. He has over 9 years of energy high yield, distressed, and equity experience. Prior to BlackGold, he was in graduate school at Tulane University. While at Tulane, he was the Associate Director of Research at Burkenroad Reports, an equity research program at Freeman School of Business. Prior to Tulane, he worked as an equity analyst at Khandwala Integrated Financial Services, a brokerage firm in India. Mr. Patel graduated from Tulane University with a master's degree specializing in Finance and Energy and holds a Bachelor of Science in management concentrating in Information Technology from Gujarat University.

|

| Shalin Patel |

No comments:

Post a Comment