You invest in factors, just make sure

they’re the right ones

By Michael Hunstad, guest columnist

Active or passive, fundamental or quantitative, domestic or international, developed or emerging, the result is the same. Whether you know it or not, your portfolio contains factor exposure. Even if your equity lineup consists of one simple allocation to the S&P 500 Index, you are still very much a factor investor.

THE OPPOSITE OF GOOD IS BAD

Today, much of the investment community recognizes that factors such as small size, high value, high momentum, low volatility, high quality, and high dividend yield have historically outperformed cap-weighted benchmarks. But, somewhat surprisingly, the converse has not been widely received — that large size, low value, low momentum, high volatility, low quality and low dividend yield logically underperformed these same cap-weighted benchmarks.This oversight is not insignificant. Exhibit 1 details the factor exposure of the S&P 500 Index, with the color coding indicating if it is positively (green) or negatively (red) compensated. As a large-cap benchmark, the S&P 500 has a large size bias with a 0.23 exposure to size but, as noted above, this large size bias has been a drag on performance. Over the long-term, this degree of exposure has drained about 45 basis points of annual return versus a portfolio with a neutral size exposure.

|

| Click image to enlarge. |

|

| Click image to enlarge. |

WHAT TO DO ABOUT THOSE LURKING FACTORS

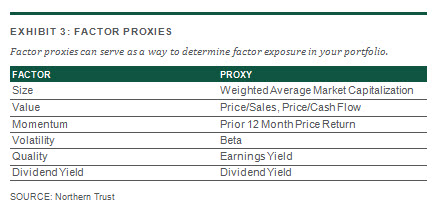

Of course, the problem is not isolated to passive and growth managers. Value, core, income, sector-specific, long-short, all types of equity investments have some, potentially quite extensive, factor exposure. To optimize performance you must be cognizant of these unintended risks and manage them appropriately. Fortunately, you don’t need access to a risk model to gauge factor content. Exhibit 3 details readily available factor proxies that can serve as a guide in determining factor exposure. |

| Click image to enlarge. |

To address the negative factor biases inherent in the Russell 1000 Growth Index, we might pair it with a strategy aimed at higher quality, higher dividend yield, lower volatility, higher value and smaller size. The goal is to create a blend of strategies to produce a portfolio with positive exposure to all factors. That would eliminate the drag of negatively compensated factor exposure and maximize positively compensated biases.

GAUGE YOUR EXPOSURE

All investors are factor investors — the key is to recognize factor exposures have major implications for investment outcomes. With the tools detailed above, asset owners can quickly and easily gauge the factor content of their portfolios and identify complementary strategies that help maximize the good and minimize the unintended risks.The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of Northern Trust Asset Management or TEXPERS.

Michael Hunstad is the head of Quantitative Strategies at Northern Trust Asset Management. Prior to joining Northern, Hunstad was head of research at Breakwater Capital, a proprietary trading firm and hedge fund. Other roles included the head of quantitative asset allocation at Allstate Investments, LLC and quantitative analyst with a long-short equity hedge fund. Michael holds a doctorate in mathematics, a master's degree in economics and a master's degree in quantitative finance.

No comments:

Post a Comment